The article identifies five high-growth nutraceutical segments in Europe – dietary supplements, probiotics, functional foods, vitamins, and sports nutrition – presenting opportunities for non-EU buyers seeking rapid market entry.

- European nutraceutical market offers high-growth potential.

- Dietary supplements lead growth, driven by aging population.

- Probiotics exhibit double-digit growth in Europe.

- Functional foods capitalize on microbiome trends.

- Ready-to-brand SKUs facilitate rapid market entry for non-EU buyers.

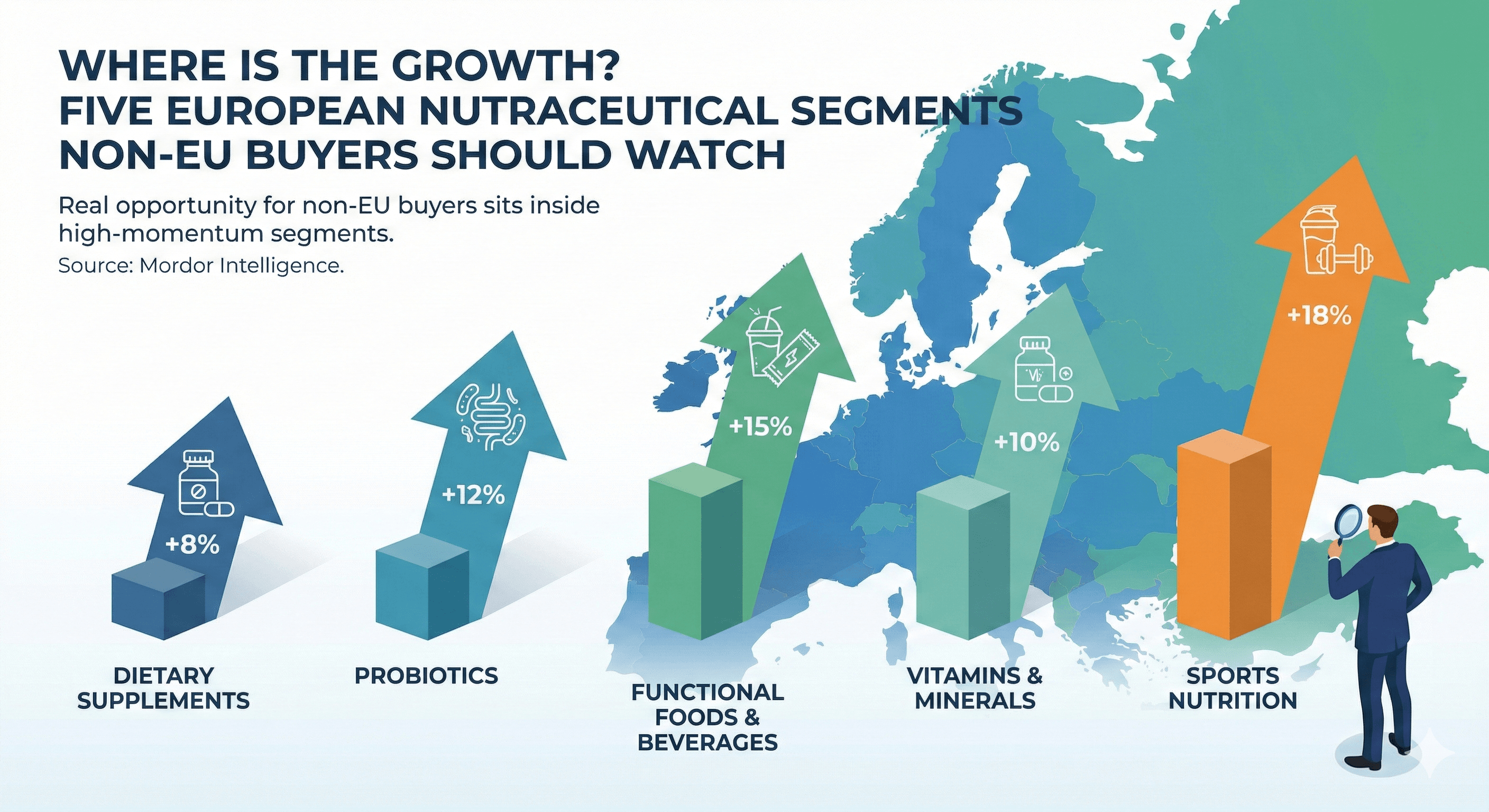

Where Is the Growth? Five European Nutraceutical Segments Non‑EU Buyers Should Watch

Europe’s nutraceutical market is expanding fast, but the real opportunity for non‑EU buyers sits inside a handful of high‑momentum segments: dietary supplements, probiotics, functional foods and beverages, vitamins and minerals, and sports nutrition. Mordor Intelligence confirms this strong trajectory.

1. Dietary Supplements: Your Fastest‑Growing “Engine Room”

Dietary supplements are the fastest‑growing type within European nutraceuticals, with many forecasts putting their growth in the 6.7–8.5% CAGR range—comfortably above the overall market pace. Mordor Intelligence and Verified Market Research both highlight this acceleration.

This growth is driven by an ageing population, rising preventive‑health habits and strong pharmacy and online channels, which together make supplements the “engine room” of European nutraceutical sales, according to Business Market Insights.

For non‑EU buyers, this segment is attractive because European manufacturers already offer a wide spectrum of compliant, ready‑to‑brand SKUs—capsules, tablets, gummies, sachets—that can be adapted quickly for local regulations and languages without redesigning the formulation from zero. Grand View Research emphasises this supply‑side flexibility.

2. Probiotics and Gut‑Health: Double‑Digit “Hero” Products

Probiotics and gut‑health products stand out as a double‑digit growth pocket: some projections put probiotic ingredients on track to reach around USD 3.1 billion by 2035, with market growth rates above 10% annually in Europe. Future Market Insights and MarkSpark Solutions both report this trajectory.

This covers probiotic and synbiotic supplements, but also yogurts, fermented drinks and gut‑health shots, making “microbiome” benefits visible on mainstream shelves rather than only in pharmacies. Mordor Intelligence provides a detailed breakdown of this retail shift.

For buyers outside Europe, the strategic value is clear: you can piggy‑back on EU‑generated clinical evidence, quality standards and strain documentation, then localise claims and positioning for your own consumers instead of trying to build scientific credibility from scratch.

3. Functional Foods & Beverages: Biggest Revenue, Strong Storytelling

Functional foods and beverages still command the largest revenue share in Europe, led by probiotic yogurts, fortified dairy alternatives, fibre‑rich snacks and protein‑enriched foods. Market Data Forecast and Cognitive Market Research detail this dominance.

European shoppers are comfortable paying a premium when they see clear added benefits—digestive comfort, immune support, energy, satiety—which gives this segment strong price‑mix potential compared with purely “indulgent” categories. foodcircle analyses this consumer willingness to pay.

For non‑EU buyers, the opportunity is to treat Europe as your source of functional bases, premixes and technology (e.g. instant functional starches, protein systems, fibre blends) and then plug those into RTE/RTC concepts that reflect local flavours, price points and eating habits.

4. Vitamins & Minerals: Resilient Core You Can Scale

Vitamins and minerals are the backbone of the European supplements market, typically holding around 28–30% of total supplement revenues thanks to their role in immunity, energy and deficiency management. Fortune Business Insights and IMARC confirm this resilient share.

Core formats like multivitamins, vitamin D, C and zinc products have benefited from post‑pandemic immunity awareness and remain a default purchase for families and older consumers. TechLabs Europe notes the sustained demand.

For non‑EU buyers, this category is a low‑risk way to expand into “European made” health products: formulations are well understood by regulators, easy to register in many markets, and can be offered under both mass and premium brands with relatively small adaptation costs.

5. Sports Nutrition & Performance: Young, Digital and Fast‑Moving

Sports nutrition and performance products—protein powders, RTD shakes, bars, energy and recovery drinks and weight‑management formulas—are among the fastest‑growing European nutraceutical segments, helped by younger consumers and e‑commerce‑driven distribution. Precedence Research and IMARC highlight this digital‑first momentum.

This segment is steadily moving from niche “gym” positioning to mainstream lifestyle branding, linking protein and performance with beauty, mental focus and everyday vitality rather than purely muscle gain. TechLabs Europe describes this rebranding.

For non‑EU buyers, European sports‑nutrition manufacturers offer high‑spec formulations, advanced protein blends and compliant claim sets that can be localised for your own digital ecosystem—especially if you sell heavily through marketplaces and D2C channels.

What This Means for Non‑EU Buyers

Across these five segments, Europe is investing in capacity, R&D and regulatory work that non‑EU buyers can effectively “rent” instead of building alone: you import finished products or functional ingredients, then apply your knowledge of local consumers, channels and price architecture.

The question for non‑EU brands is not whether European nutraceuticals are growing—they clearly are—but which of these high‑momentum segments you want to own in your market, and how quickly you can turn EU supply into distinctive, trusted products on your shelves.